Listen to this Blog

🧬 Anthem Biosciences IPO Analysis: Should You Subscribe?

IPO Price Band: ₹570 per share

Issue Size: ₹— 3395 Cr

Sector: Biopharmaceutical Contract Research & Manufacturing (CRAMS)

Listing: NSE, BSE

IPO Opening: 14th July 25 | Closing: 16th July 25

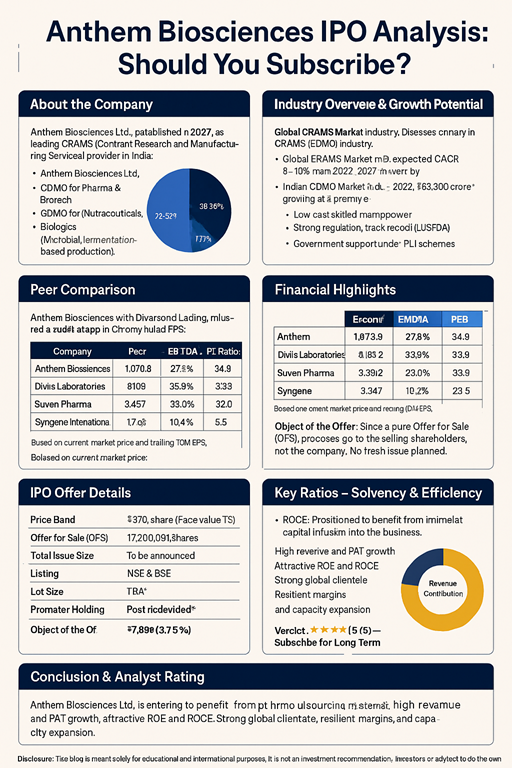

🔬 About the Company

Anthem Biosciences Ltd., established in 2007, is a leading CRAMS (Contract Research and Manufacturing Services) provider in India. It offers end-to-end solutions, including:

Research & Development (discovery to scale-up)

Intermediates and APIs

Finished formulations (nutraceuticals, injectables, etc.)

Biological and biosimilar research

Key Business Segments:

CDMO for Pharmaceuticals

CDMO for Nutraceuticals

Biologics (Microbial fermentation-based production)

With 4 state-of-the-art manufacturing facilities in Bangalore, Anthem has built strong relationships with over 1,100 global clients from 90+ countries.

Revenue Contribution (FY23):

🌍 Industry Overview & Growth Potential

Anthem operates in the CRAMS (CDMO) industry, which is witnessing robust growth globally and in India.

Global CRAMS Market:

Size (2022): $130 billion

Expected CAGR (2022–2027): 8–10%

Drivers: Outsourcing by Big Pharma, focus on cost reduction, need for faster time-to-market

Indian CDMO Market:

Size (2022): ₹65,300 crore

Expected to grow at CAGR of 11–13%

India is becoming a preferred CDMO hub due to:

Low-cost skilled manpower

Strong regulatory track record (USFDA approvals)

Government support under PLI schemes

🧭 Peer Comparison

*Based on current market price and trailing 12M EPS.

Anthem shows competitive profitability and stronger ROCE than many peers, offering attractive financial fundamentals.

📦 IPO Offer Details

👇 Object of the Offer:

Since it's a pure Offer for Sale (OFS), proceeds go to the selling shareholders, not the company. No fresh issue is planned.

💹 Financial Highlights

Revenue & Profit Growth (₹ Crore)

3-Year CAGR (FY21–FY23):

Revenue: 34.4%

PAT: 57.6%

🧮 Valuation at ₹570:

Though the P/E is high above peers, the high growth, margin expansion, and ROE support this premium. However Divislab is the best among all the companies considering Market size, Solvency and other parameters.

⚖️ Key Ratios – Solvency & Efficiency

Anthem maintains a strong solvency position with low debt and efficient capital usage.

📌 Basis for the Offer

Fast-growing Indian CDMO with 3-year CAGR of 34% in revenue and 58% in PAT.

High-margin business with increasing capacity and client base.

Strong financial discipline and consistent profitability.

Positioned to benefit from global pharma outsourcing wave and China+1 strategy.

Scalable model with plans for biologics and fermentation scale-up.

✅ Conclusion & Analyst Rating

Anthem Biosciences Ltd. is entering the public markets at a time when pharma outsourcing is gaining momentum. With:

Not a leader, Divis Labs wins here.

High revenue and PAT growth

Attractive ROE and ROCE

Strong global clientele

Resilient margins and capacity expansion

… it presents a strong investment case for long-term investors.

🔖 Verdict: ⭐️⭐️⭐️⭐️☆ (4/5) — Subscribe for Long-Term

While the absence of fresh issues limits immediate capital infusion into the business, the fundamentals remain compelling. Here Divis gets 4.5 Star rating.

📢 Disclosure:

This blog is meant solely for educational and informational purposes. It is not an investment recommendation. Investors are advised to do their own due diligence before making investment decisions.

.jpg)