Listen to this Blog

📰 Key Highlights – CPI July 2025

-

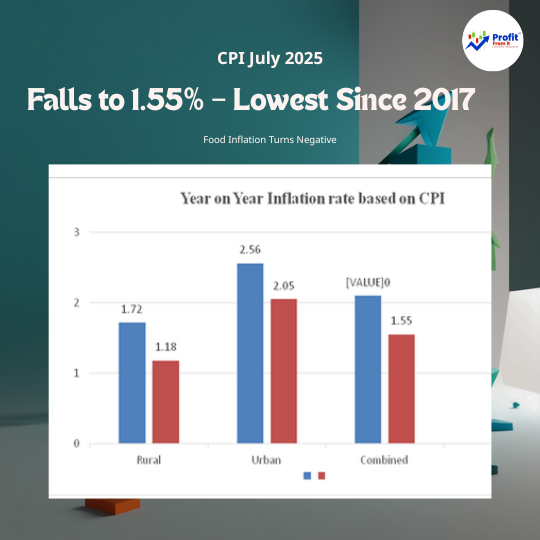

Headline CPI Inflation: 1.55% YoY (lowest since June 2017) vs 2.10% in June 2025.

-

Food Inflation (CFPI): -1.76% YoY, lowest since Jan 2019.

-

Rural Inflation: 1.18% | Urban Inflation: 2.05%.

-

Major contributors to decline: Pulses, Vegetables, Cereal Products, Education, Eggs, Sugar, Transport & Communication.

-

Housing Inflation: 3.17% | Education Inflation: 4.00% | Health Inflation: 4.57%.

-

Fuel & Light Inflation: Slight uptick to 2.67%.

📊 Sector Analysis & Key Observations

| Sector | Current Inflation Trend | Impact |

|---|---|---|

| FMCG – Food Products | Negative food inflation (-1.76%) | Margin expansion possible due to lower raw material costs; rural demand may improve. |

| Auto & Transportation | Transport inflation down to 2.12% | Fuel stability + lower logistics costs → positive for auto OEMs, logistics firms. |

| Real Estate & Housing | Housing inflation steady at 3.17% | Controlled inflation supports stable EMIs; positive for residential demand. |

| Education Services | Decline to 4.00% from 4.37% | Tuition fee growth slowing; may affect revenue growth for edu-companies. |

| Healthcare | Marginal increase to 4.57% | Medical cost pressure persists; hospital chains may maintain pricing power. |

| Energy – Fuel & Light | 2.67% vs 2.55% | Slight rise; minimal impact on industrial energy costs. |

🏢 How This Impacts Companies

Potential Beneficiaries

-

FMCG Players (HUL, Nestle, Britannia) – Lower food inflation reduces input cost pressures, supporting margins.

-

Auto Manufacturers (Maruti, Tata Motors) – Lower logistics & fuel-related inflation boosts affordability & demand.

-

Retail Chains (DMart, V-Mart) – Lower food prices + improved rural demand likely to support volume growth.

-

Real Estate Developers (DLF, Godrej Properties) – Stable housing inflation keeps affordability intact, supporting sales momentum.

Caution for Investors

-

Agribusiness & Fertilizers – Negative food inflation may hurt farm income in the short term.

-

Education Providers – Slower inflation in fees may cap revenue growth.

-

Healthcare Chains – Rising medical inflation may draw regulatory scrutiny.

📈 Stock Market Outlook

Short Term (3–6 months)

-

Lower inflation → higher probability of RBI maintaining accommodative stance, supportive for equities.

-

FMCG, Auto, and Realty could outperform.

Medium to Long Term (1–3 years)

-

Sustained low inflation can boost consumption but may weigh on rural incomes if farm-gate prices remain weak.

-

Defensive sectors (FMCG, Pharma) remain attractive; cyclicals (Auto, Infra) could gain if demand improves.

🔍 Long-Term Watch (2025–2030)

-

Structural Trend: If India maintains inflation in 2–4% range, it could enable stable interest rates & long-term economic planning.

-

Sectors to Watch: Consumption (FMCG, Retail), Affordable Housing, Logistics, E-commerce.

-

Risks: Prolonged negative food inflation could depress rural income and slow agri-related consumption.

📌 Key Takeaways

-

CPI at 1.55% = lowest in 8 years → market positive.

-

Food prices falling sharply → benefits urban consumers, challenges rural incomes.

-

Multiple sectors stand to gain from reduced cost pressures.

.jpg)