Listen to this Blog

India’s Next‑Generation GST Reforms –

Official Press Release Insights and Investment Implications

Published: 3 September 2025

Author: Piyush Patel

Introduction

The Goods & Services Tax (GST) Council’s 56th meeting on 3 September 2025 delivered the most sweeping restructuring of the indirect tax regime since GST’s launch in 2017. A detailed press release issued at 8 p.m. on the same day lays out HSN‑wise and sector‑wise rate changes across hundreds of goods and services. The reforms simplify compliance, provide targeted relief to consumers and businesses, and introduce a high sin‑goods rate to curb consumption of harmful products.

The Council recommended implementing the new rates from 22 September 2025 for most goods and services. Pan masala, gutkha, cigarettes, chewing tobacco, unmanufactured tobacco and bidi will continue at existing rates until liabilities under the compensation‑cess account are settled. The press release also mandates that 90 % of refund claims arising from inverted duty structures be provisionally sanctioned based on risk analysis.

This blog distils the voluminous annexures into investor‑friendly themes, highlighting key rate changes, sectoral winners and losers, and what the reforms mean for listed companies.

Major GST Rate Changes on Goods

The press release lists over 100 HSN codes with rate alterations. To aid investors, the changes can be grouped into broad categories:

Key GST Changes on Services

The Council also rationalised GST rates on several service categories:

Process & Legal Reforms

Beyond rate changes, Annexure V recommends a series of process reforms to improve compliance and ease of doing business:

Risk‑based provisional refunds: The Council endorsed sanctioning 90 % of refund claims related to zero‑rated supplies and inverted duty structures based on system‑generated risk evaluation. This will improve working‑capital flow for exporters and businesses facing inverted duty situations.

Simplified GST registration: A proposed optional simplified registration scheme grants automatic registration within three working days to low‑risk applicants whose expected output tax liability on supplies to registered persons does not exceed ₹2.5 lakh per month. This scheme, expected to benefit 96 % of new applicants, will be operational from 1 November 2025.

Simplified registration for small e‑commerce suppliers: The Council approved, in principle, a simplified mechanism allowing small suppliers on e‑commerce platforms to register without maintaining a principal place of business in each state, easing compliance for cross‑state sellers.

Place of supply for intermediary services: Clause 13(8)(b) of the IGST Act is proposed to be omitted, aligning place of supply for intermediary services with the location of the recipient. This would classify such services as exports, enabling exporters to claim benefits.

Post‑sale discount clarifications: Sections 15 and 34 of the CGST Act will be amended to simplify treatment of post‑sale discounts. Clarification will also be issued on non‑reversal of input tax credit when discounts are provided via financial/commercial credit notes.

Retail sale price valuation for pan masala and tobacco: GST will be levied on the retail sale price rather than transaction value for pan masala, gutkha and tobacco products, ensuring better valuation and tax capture.

GSTAT operationalisation: The Goods and Services Tax Appellate Tribunal (GSTAT) will become operational by end‑September 2025, with hearings beginning before the end of December. The principal bench will also act as the National Appellate Authority for advance rulings.

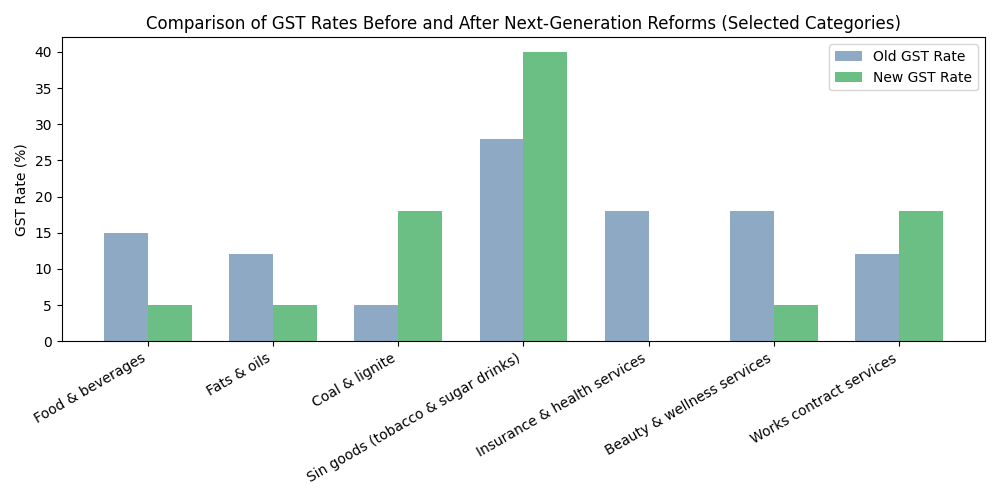

Visualising the New Rate Landscape

The following chart compares approximate average GST rates before and after the reforms across representative categories of goods and services. It highlights rate cuts (e.g., food, fats & oils), exemptions (insurance services) and increases (coal & lignite, sin goods, works contracts).

Sectoral Impact & Investment Outlook

Sectors Likely to Benefit

Sectors Facing Headwinds

Positive Outcomes

Broader consumption stimulus: Substantial rate cuts on food, FMCG, fats, oils, chemicals and handicrafts will lower prices and enhance affordability, especially for the middle class and rural consumers.

Push for environmental and health services: Reduced GST on effluent and biomedical waste treatment encourages compliance and investment in environmental infrastructure. Exemption for life and health insurance will help deepen insurance penetration and healthcare access.

Support for MSMEs and artisans: Simplified registration, provisional refunds and lower rates for handicrafts and small suppliers will foster the formalisation and growth of MSMEs.

Tax clarity and institutional strengthening: The operationalisation of GSTAT and clarifications on post‑sale discounts provide greater legal certainty and trust in the GST regime.

Broader consumption stimulus: Substantial rate cuts on food, FMCG, fats, oils, chemicals and handicrafts will lower prices and enhance affordability, especially for the middle class and rural consumers.

Push for environmental and health services: Reduced GST on effluent and biomedical waste treatment encourages compliance and investment in environmental infrastructure. Exemption for life and health insurance will help deepen insurance penetration and healthcare access.

Support for MSMEs and artisans: Simplified registration, provisional refunds and lower rates for handicrafts and small suppliers will foster the formalisation and growth of MSMEs.

Tax clarity and institutional strengthening: The operationalisation of GSTAT and clarifications on post‑sale discounts provide greater legal certainty and trust in the GST regime.

Potential Risks & Considerations

Fiscal impact and compensation cess: Large rate cuts could strain tax revenues in the short term. Sin‑goods increases may not fully offset losses, and compensation cess obligations must be settled before pan masala and tobacco rates are lowered.

Inflationary pressure in energy and sin segments: Higher GST on coal and lignite could raise energy costs, impacting power tariffs and downstream industries. Consumers of pan masala, sugary drinks and tobacco will bear higher costs, potentially fuelling inflation in discretionary categories.

Implementation complexity: Businesses must update pricing, IT systems and accounting to reflect the new rates. The phased implementation (22 September 2025) and exceptions for sin goods add complexity.

Sector‑specific demand elasticity: Some rate increases (works contract, aviation, casinos) may significantly curb demand, affecting volumes and profitability.

Fiscal impact and compensation cess: Large rate cuts could strain tax revenues in the short term. Sin‑goods increases may not fully offset losses, and compensation cess obligations must be settled before pan masala and tobacco rates are lowered.

Inflationary pressure in energy and sin segments: Higher GST on coal and lignite could raise energy costs, impacting power tariffs and downstream industries. Consumers of pan masala, sugary drinks and tobacco will bear higher costs, potentially fuelling inflation in discretionary categories.

Implementation complexity: Businesses must update pricing, IT systems and accounting to reflect the new rates. The phased implementation (22 September 2025) and exceptions for sin goods add complexity.

Sector‑specific demand elasticity: Some rate increases (works contract, aviation, casinos) may significantly curb demand, affecting volumes and profitability.

Conclusion

The official press release on next‑generation GST reforms reveals a comprehensive overhaul of India’s indirect tax landscape. The shift to lower rates for a wide range of food items, edible oils, chemicals, handicrafts, environmental services and certain transport services will likely spur consumption and investment. Meanwhile, sharp hikes on sin goods, coal and high‑value services signal the government’s intent to promote healthier lifestyles and raise revenue from non‑essential activities.

For investors, the reforms create clear tailwinds for FMCG, edible oils, pharmaceuticals, environment services, hospitality, beauty & wellness and handicrafts, while posing headwinds for sin‑goods producers, coal miners, premium transport providers and gaming companies. Thorough due diligence on company fundamentals, demand elasticity and regulatory compliance remains crucial. Overall, the GST overhaul underlines the government’s commitment to simplifying taxes and stimulating growth, presenting opportunities for well‑positioned companies and informed investors.

.jpg)