## 🌍 **Global Economic Landscape: Snapshot and Trajectory**

The dataset outlines historical and projected nominal GDP (in current US$) for the top 50 economies from 1960 to 2030. It also includes:

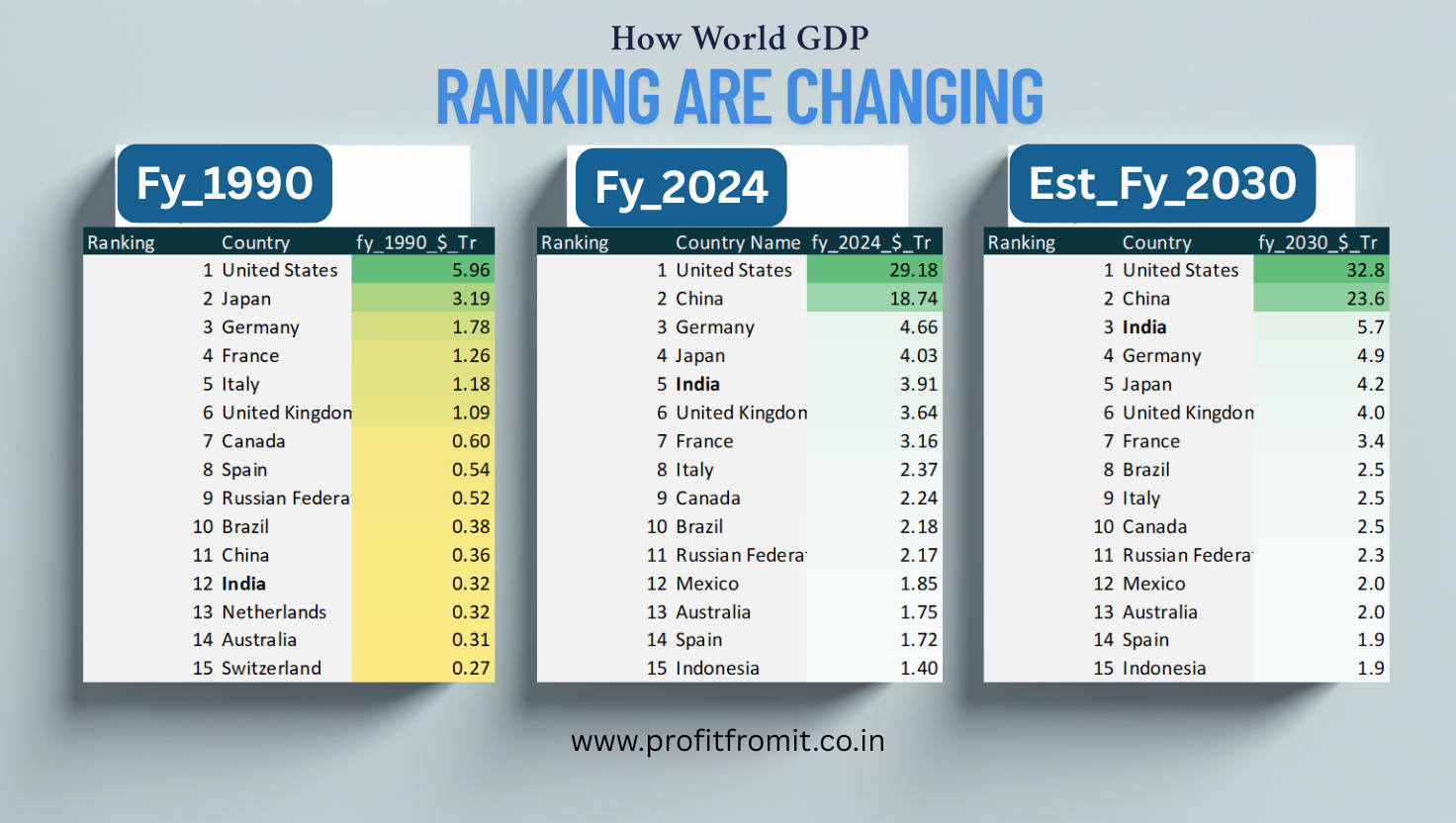

- GDP rankings in **1990**, **2024 (estimated)**, and **2030 (projected)**

- Annual **GDP growth rates** for 2025–2030

- Underlying data from **World Development Indicators**

#### 🥇 **Key Shifts in Global Economic Power**

| Rank Shift | 1990 → 2030 | Commentary |

|------------|-------------|------------|

| **China** | #11 → #2 | Overtook Japan (2010s); closing in on the US in nominal terms |

| **India** | #12 → #3 | Outpaces Japan and Germany by 2030 with projected $5.68T GDP |

| **Indonesia** | #29 → #15 | Signals emergence of ASEAN as a global growth cluster |

| **Bangladesh** | #47 → #29 | Reflects strong demographic tailwinds and productivity base |

| **Russia** | #9 → #11 | Slips two spots despite strong rebound from commodity cycles |

| **UK** | #6 → #6 | Holds position but slower growth than Asian counterparts |

| **Japan** | #2 → #5 | Structural stagnation leads to relative decline |

| **Germany** | #3 → #4 | Maintains strength but eclipsed by India |

---

### 📈 **Macro Growth Trends (2025–2030)**

| Country | Avg Growth (Est.) | Implication |

|------------------|------------------|-------------|

| **India** | 6.5% | Resilient domestic demand + digital infra; equity upside |

| **Indonesia** | 5.1% | Consumption-led growth; mid-cap play |

| **Philippines** | 6.3% | Urbanization & services export potential |

| **China** | ~3.8–4.2% | Moderating as economy matures; structural rebalancing |

| **US** | ~2% | Stable but mature; sector rotation matters |

| **Germany/Japan**| ~1–1.2% | Defensive sectors preferred; aging demographics |

---

### 📊 **Implications for Equity Investors**

#### ✅ **Opportunities**

- **Thematic Alpha**: India, Indonesia, Vietnam and the Philippines offer compelling growth with market-friendly reforms and rising middle-class consumption.

- **Sectoral Exposure**:

- **Financials & Infra** in India and Indonesia

- **Consumer Discretionary & Tech Exports** in ASEAN

- **Defense & Renewables** in US, Germany, and France

- **Frontier Upgrades**: Bangladesh and Vietnam may progress from frontier to emerging status, attracting passive flows.

#### ⚠️ **Risks**

- **Developed Markets Rotation**: US & EU equities could face valuation compression as capital reallocates to high-growth EMs.

- **Geopolitical Realignment**: Supply chain shifts, tariffs, and defense spending may redefine "resilience" and pricing power.

- **Currency Volatility**: Nominal GDP growth may not translate into dollar returns; hedge accordingly.

---

### 📌 **Recommended Investor Actions**

| Time Frame | Action Plan |

|------------------|-------------|

| **Short-Term (1–2 yrs)** | Monitor reforms (India’s CapEx cycle, China stimulus, EU Green Deal); use dips to accumulate EM ETFs |

| **Mid-Term (3–5 yrs)** | Build exposure to **Asia-focused multi-thematic funds**—digitization, infra, green mobility |

| **Long-Term (>5 yrs)** | Strategic allocations to countries with strong **GDP per capita growth + demographic tailwinds** (e.g., India, Indonesia, Vietnam) |

---

### 🧭 **Conclusion: Tilt Toward Growth with Guardrails**

The next global economic frontier is unmistakably **Asian-led**. But nominal GDP is only part of the story—**investability hinges on policy stability, FX management, depth of capital markets, and corporate governance**.

👉 **A barbell strategy combining growth EMs (India, ASEAN) and resilient DMs (US, select EU sectors) ensures diversification across cycles**.