Bharat Electronics Limited (BEL) Q1 FY26 Results Analysis 📊

Current Market Price: ₹377

Report Date: July 28, 2025

1. Recent Insights & Highlights 🔍

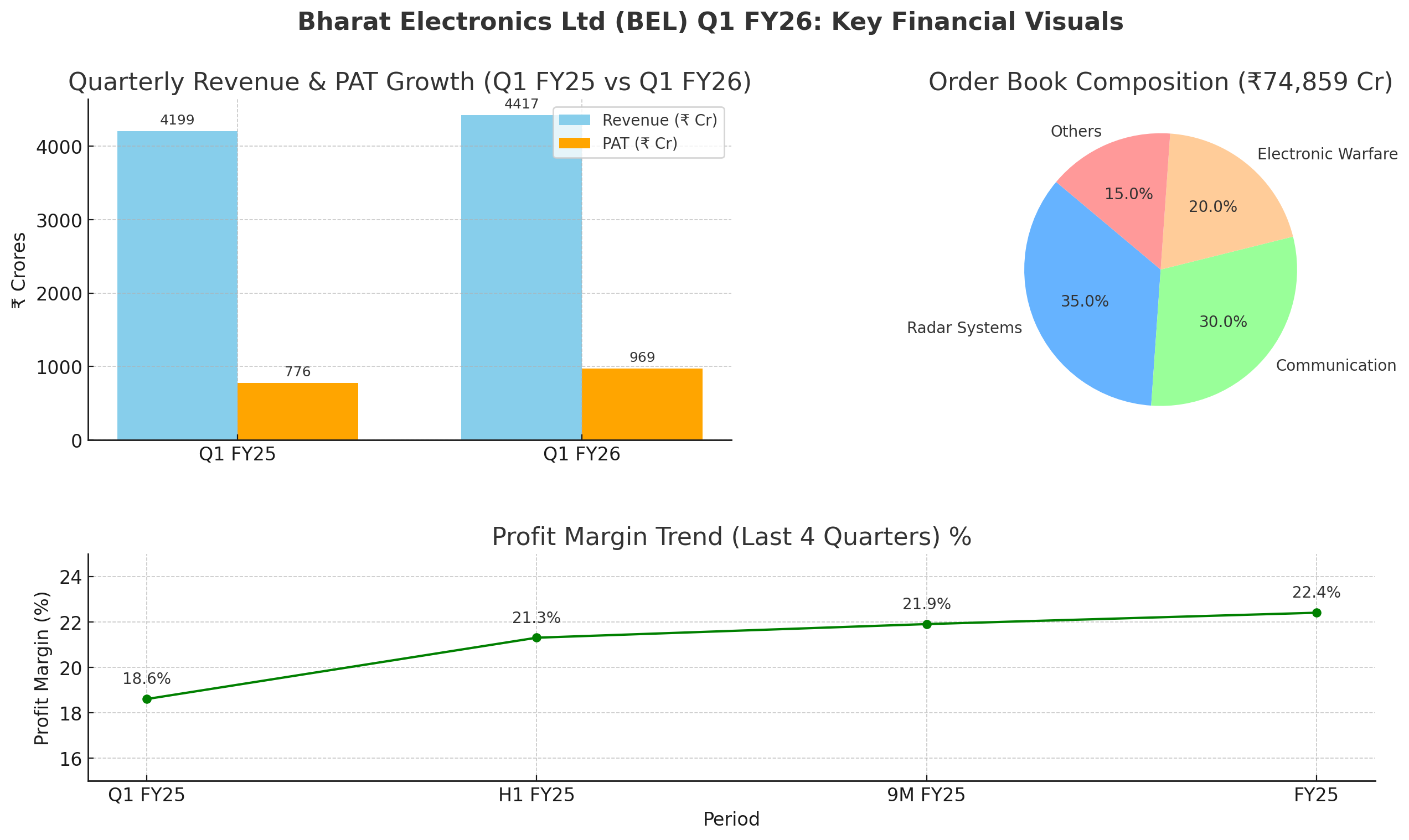

Revenue Growth: BEL reported Revenue from Operations of ₹4,416.83 crore in Q1 FY26, marking a 5.19% increase YoY compared to ₹4,198.77 crore in Q1 FY25.

Profitability: Profit Before Tax (PBT) stood at ₹1,289.24 crore, growing 24.28% YoY, while Profit After Tax (PAT) was ₹969.13 crore, up 24.87% YoY.

Order Book Strength: The company maintains a robust order book of ₹74,859 crore as of July 1, 2025, providing strong revenue visibility for the medium term.

Strategic Context: Despite geopolitical tensions (e.g., conflicts in Israel), management confirms no material financial impact on contracts. Dividend policy continues to reward shareholders with an interim and final dividend totaling 240%.

2. Consolidated Financial Analysis 💼

Note: Margins calculated as PAT / Revenue.

3. Profitability & Valuation Ratios 📈

*Based on Trail EPS and current market price

4. Industry-Specific KPIs & Growth Trend ⚙️

As a defense PSU, BEL's key strength lies in its strong order book and execution capabilities rather than typical IT or consumer KPIs. Key growth drivers:

Order Book: ₹74,859 crore (very healthy for revenue visibility)

Sales Growth: Moderate YoY sales growth at 5.19% reflects steady demand.

Profit Growth: Robust profit growth near 25% YoY reflects operational efficiencies and cost control.

Historical Quarterly Growth Trend (FY25)

5. Near-Term & Long-Term Outlook 🔮

Near-Term (Next 1-2 Quarters):

Management guidance is optimistic with a strong order book ensuring steady revenue growth. Continued focus on project execution and supply chain management amid global uncertainties remains key.Long-Term (FY26 and Beyond):

BEL is well-positioned to benefit from rising defense budgets and indigenization drives under "Make in India." Expansion in emerging technologies like electronic warfare, radar systems, and communication equipment can fuel sustained growth.

6. Conclusion for Long-Term Investors 🏦

Key Positives:

Solid revenue and profit growth with healthy margins.

Strong order book of ₹74,859 crore offering revenue visibility.

Dividend payouts remain attractive.

Government backing as a Navratna PSU supports stability.

Potential Risks:

Geopolitical uncertainties could impact some contracts.

Moderate sales growth may concern growth-focused investors.

High P/E ratio suggests valuation premium; caution advised on market price volatility.

Overall Stance:

Cautiously Optimistic — BEL remains a dependable defensive stock with steady profit growth and strong government orders, suitable for long-term portfolios emphasizing stability and dividend income.

7. Disclosure 📢

This analysis is provided solely for informational purposes and does not constitute investment advice. Investors should perform their own due diligence before making investment decisions.