Asian Paints Q1 FY26 Results: Analysis with Key Insights & Outlook 🏭🎨

Current Market Price (CMP): ₹2,437

1. Recent Insights and Highlights 📢

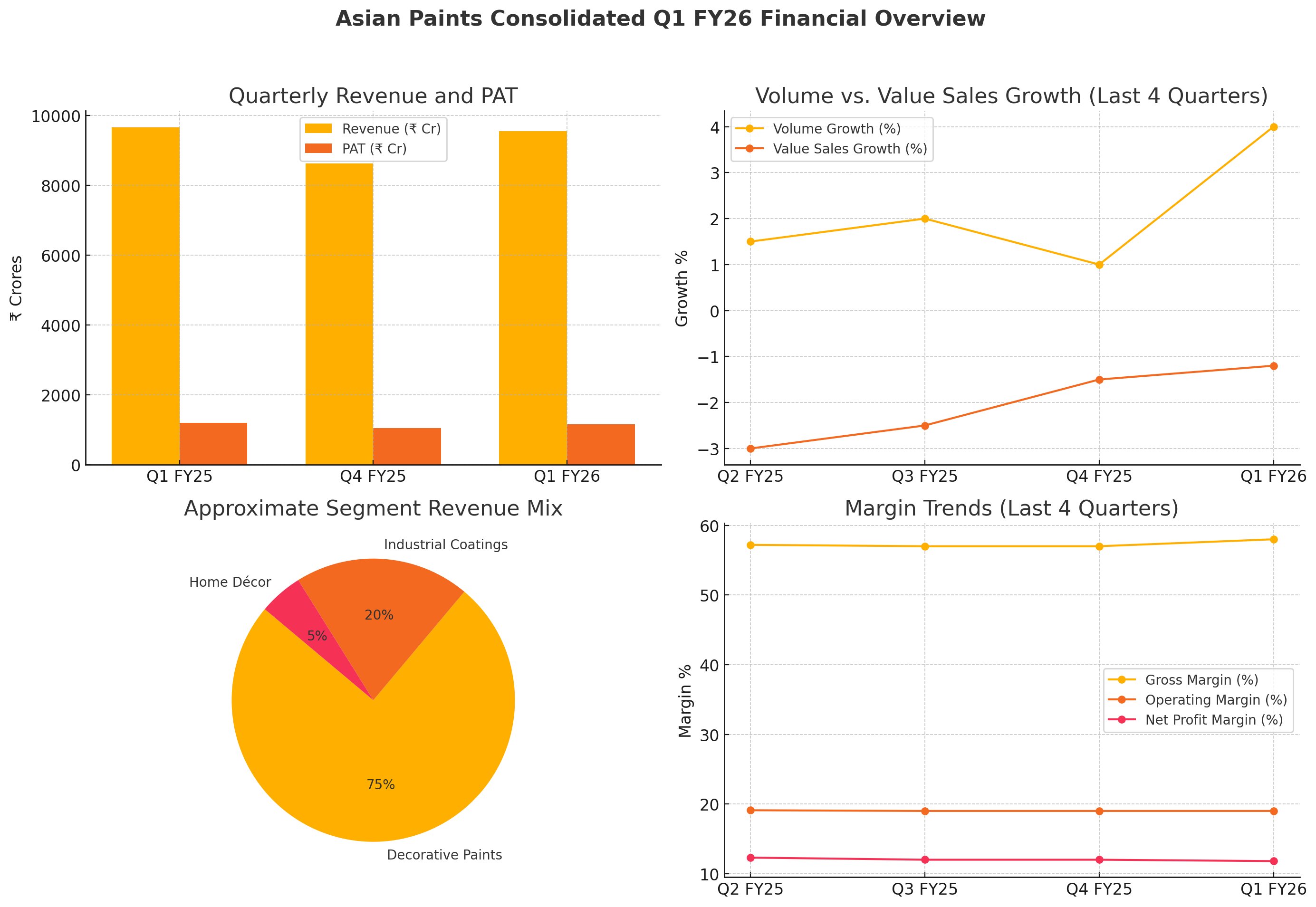

Volume recovery in decorative paints: Asian Paints’ decorative segment volume grew by about 4%, showing signs of demand revival after subdued quarters.

Value sales slightly negative: Value declined by around 1.2%, indicating continued pricing pressures and some consumer downtrading.

Industrial segment remains strong: Industrial coatings, including auto and marine segments, grew robustly at ~11%.

Monsoon impact: Early monsoon rains affected exterior painting activities in June, tempering demand.

Innovation-led growth: New products contributed ~14% to consolidated revenues, with focus on premium ranges like Nilaya Arc.

Distribution network expansion: Consolidated reach expanded to approximately 170,000 retail outlets, strengthening market presence.

Home Décor business under pressure: Discretionary spending slowdown continues to affect modular kitchens and bath fittings.

Strategic backward integration: Major CapEx projects on emulsion and white cement plants progressing well to enhance cost efficiency and product differentiation.

2. Consolidated Financial Analysis 📊

Margins (%)

*Estimated from revenue and cost of materials consumed.

3. Profitability & Valuation Ratios 🔍

*Estimated based on recent annual reports.

4. Industry-Specific KPIs & Segment Highlights 🎯

Decorative Paints: Volume growth of ~4%, value sales down marginally by 1.2%, impacted by competitive pricing.

Industrial Coatings: Strong double-digit volume growth (~11%), driving overall segmental growth.

Home Décor: Still under pressure, affected by discretionary spend reduction and segment losses.

Distribution: Expanded retail presence to 170,000 outlets across India and consolidated markets.

Innovation: New product contribution steady at 14% revenue share, emphasizing premium and differentiated products.

Backward Integration: Strategic projects progressing to reduce costs and improve product quality.

5. Near-Term & Long-Term Outlook 🔮

Near-Term (Next 1-2 Quarters)

Expect continued volume growth in decorative and industrial segments.

Pricing pressures are likely to persist, limiting value growth.

Monsoon impact expected to normalize; demand in urban and semi-urban markets may strengthen.

Home Décor business needs strategic focus to return to profitability.

Long-Term (FY27–FY30)

Backward integration investments to support margin expansion.

Strong innovation pipeline with premiumization likely to drive ASP improvement.

Expanded retail and service ecosystem to consolidate market leadership.

Favorable macro environment with increasing housing and infrastructure demand.

6. Conclusion for Long-Term Investors ✅⚠️

Positives

Solid volume growth recovery in decorative paints and industrial coatings.

New product innovation driving premium segment growth.

Expanding distribution footprint and customer service initiatives.

Backward integration projects enhancing cost competitiveness.

Risks & Challenges

Pricing and value sales under pressure due to competitive intensity.

Discretionary Home Décor segment remains weak and loss-making.

External factors like weather and economic slowdown can impact demand.

High valuation multiples limit upside in the near term.

Investment Stance

Asian Paints remains a well-managed, market-leading franchise with sustainable long-term growth drivers. Near-term headwinds on pricing and discretionary spending call for cautious optimism. Long-term investors should consider a hold or accumulate on dips strategy, watching for margin and Home Décor business improvements.

7. Disclosure 📝

This analysis is provided solely for informational purposes and does not constitute investment advice. Investors should perform their own due diligence before making investment decisions.