✈️ IndiGo Q1 FY26 Results – Navigating Headwinds, Flying Towards Growth!

CMP: ₹5,933 | Quarter Ended: 30 June 2025

📌 1. Recent Insights & Management Highlights

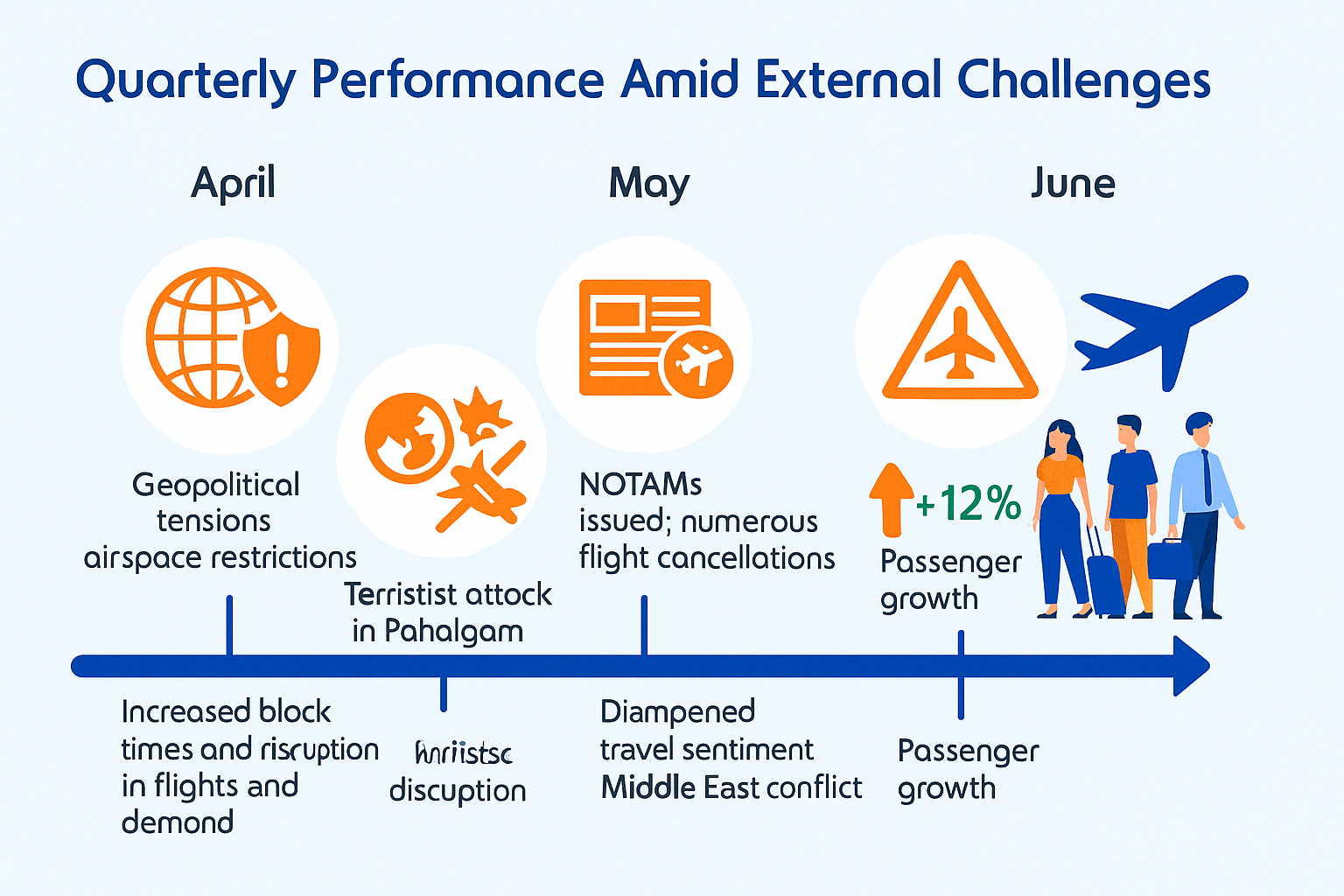

Passenger Growth: Despite geopolitical tensions, airspace restrictions, and the tragic AI171 accident, passenger count grew +11.6% YoY to 31 million, outpacing industry growth (~6%).

New International Expansion:

Launched Mumbai–Amsterdam and Mumbai–Manchester with damp-leased widebody aircraft.

Announced upcoming London & Copenhagen routes.

Strengthened codeshare partnerships with KLM, Japan Airlines, Jetstar, Delta Airlines, and Virgin Atlantic.

Domestic Growth: Added Hindon (Ghaziabad) & Adampur (Jalandhar) routes; preparing to be launch carrier at Jewar & Navi Mumbai airports.

Fleet Actions: Net decrease of 18 passenger aircraft in Q1 as damp leases returned; inducted 8 aircraft via captive leasing unit at GIFT City.

Product Innovations: Expanded premium ‘Stretch’ seating to key regional international routes; launched co-branded Kotak Mahindra Bank credit card.

Operational Reliability: On-time performance 83.4%, technical dispatch reliability 99.88%.

📊 2. Consolidated Financial Analysis

Segmental/Regional Mix:

Domestic passengers up 14% YoY; international expansion continues to build share.

Margins:

Gross Margin: Impacted by lower yields & load factor.

Operating Margin: Down due to higher airport charges, depreciation, and employee costs.

Net Margin: 10.6% (vs 13.9% last year).

📈 3. Profitability, Growth & Valuation Ratios

ROE: ~24% (annualized)

ROCE: ~18% (annualized)

EPS: ₹56.31 (quarter)

P/E (TTM): ~29x at CMP ₹5,933

📍 4. Industry-Specific KPIs – Airlines

Passenger Load Factor: 84.6% (↓ 2.1 ppt YoY)

PRASK: ₹4.21 (↓ 7% YoY)

CASK ex-fuel ex-forex: ₹2.89 (↑ 1.8% YoY)

Fuel CASK: ₹1.38 (↓ 21.9% YoY on softer fuel prices)

📊 5. FY26 Estimates (Based on Trend & Management Outlook)

📅 Historical Trend:

FY25 Sales Growth: 17% | Profit Margin: 9.0% | Profit Growth: -11%

🔮 6. Outlook

Near-Term (Q2 FY26):

Q2 seasonally weakest for domestic travel; capacity addition only mid–high single digit YoY.

Yield environment stabilizing; gradual improvement expected Aug–Sep.

Long-Term (FY27+):

Widebody expansion, new international markets, and Indian middle-class travel boom provide multi-year growth runway.

Risks: Fuel price volatility, geopolitical tensions, competition on international routes.

✅ 7. Conclusion for Long-Term Investors

Positives:

Market leadership in India with strong brand & network.

International expansion unlocking new revenue streams.

Cost efficiency culture & strong liquidity (₹49,405 Cr cash).

Risks:

Yield pressure in competitive markets.

Seasonal weakness in domestic travel.

External disruptions (geopolitics, airspace closures).

Investment Stance:

📌 Cautiously Optimistic – Attractive for long-term investors who can tolerate quarterly volatility.

📜 Disclosure

This analysis is provided solely for informational purposes and does not constitute investment advice. Investors should perform their own due diligence before making investment decisions.