🚗 Maruti Suzuki Q1 FY26 Results – Steady Profit, Strong Exports, But Margins Under Pressure

CMP: ₹12,542 | Period: April–June 2025

1️⃣ Key Management Highlights 📢

From the Earnings Concall:

Industry Trends: Domestic PV industry declined 1.4% YoY; SUV share crossed 55%, MPVs at 11%, hatchbacks fell to 21% share from 46% in FY19.

Export Leadership: Maruti commanded 47.1% of India’s total PV exports, with 37.4% YoY export growth.

Safety First: All-new Dzire became India’s first sedan with 5-star Bharat NCAP rating; Baleno scored 4-star. 97% of volumes now come with six airbags.

SUV Milestones: Grand Vitara fastest mid-SUV to hit 3 lakh sales; Fronx fastest SUV to reach 1 lakh exports in 25 months.

Sustainability Initiatives: Solar capacity at 78.2 MWp, aiming for 319 MW by FY31 (85% renewable electricity share).

Logistics Efficiency: 24.3% of dispatches via rail in FY25; target 35% by FY31.

2️⃣ Consolidated Financial Performance 💹

3️⃣ Segment & Regional Breakdown 🌏

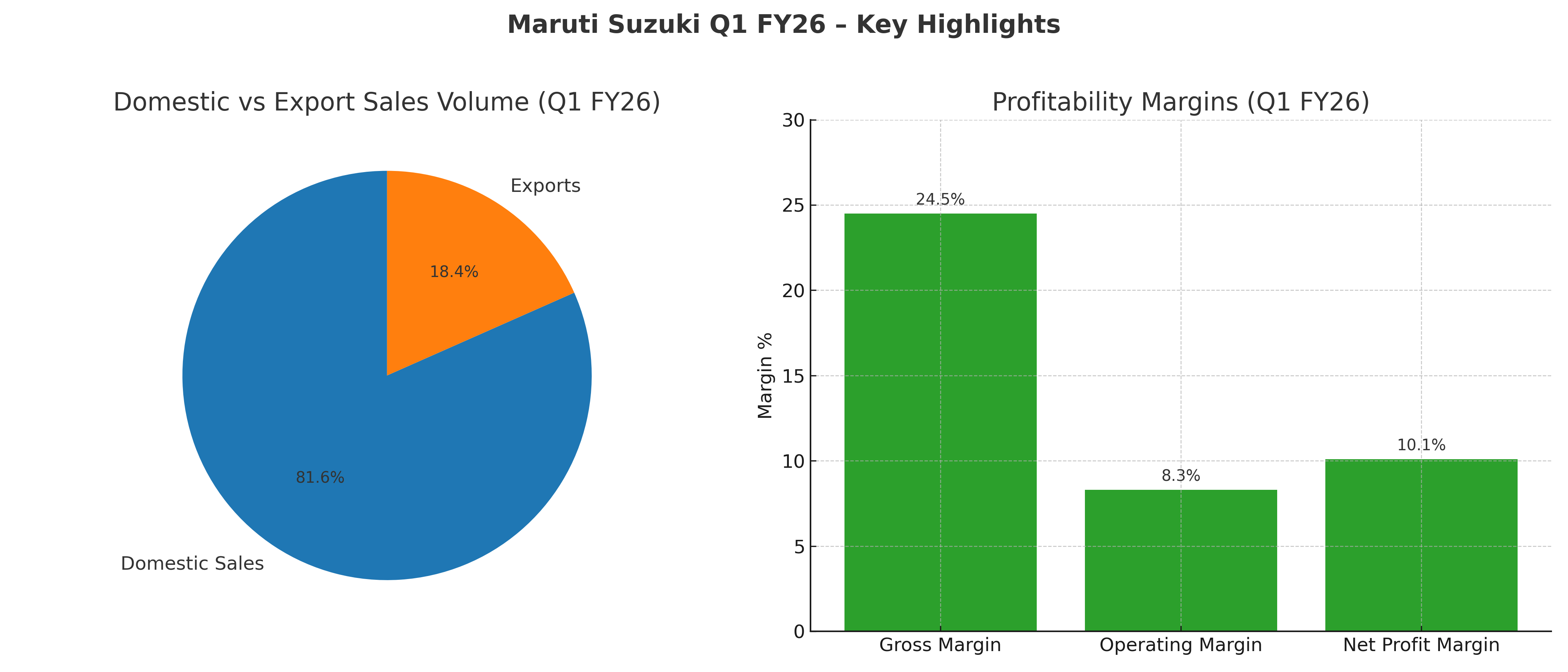

Domestic Sales – 4,30,889 units (-4.5% YoY)

Mini: 19,522 (-36.6%) ⚠️

Compact: 1,77,270 (-6.3%) ⚠️

UVs: 1,61,868 (-0.8%)

Vans: 33,105 (-2.0%)

LCV: 8,510 (+7.1%) 👍

Sales to other OEMs: +18.8% 👍

Exports – 96,972 units (+37.4% YoY) 🚀

Strong performance in Japan (now 2nd largest export market).

4️⃣ Profitability, Growth & Valuation Ratios 📊

ROE: ~14.8%

ROCE: ~19.5%

EPS (TTM): ₹462.24

P/E (CMP ₹12,542): ~27x

5️⃣ Auto Industry KPIs 🚘

Volume Growth: Domestic -4.5%, Exports +37.4%

Market Share Change: SUV & MPV gaining share, hatchback declining.

Dealer Inventory: ~33 days (well-managed).

6️⃣ FY26 Outlook Based on Trends & Guidance 📅

Near-Term (Next 1–2 Quarters)

Expect improvement during festive season; rural demand holding up 🌾.

Two new SUV launches (one EV, one ICE) expected to boost volumes.

Margins may remain under pressure due to commodity & forex headwinds.

Full Year Estimates (Based on Current Trend & 4Q Average)

Sales Growth: ~7%

Profit Margin: ~5%

Profit Growth: ~9.3%

Long-Term (FY26–FY30)

Strong export expansion (100+ countries).

Higher EV penetration; hybrid & CNG to remain important for compliance and affordability.

Solar & rail initiatives to improve cost efficiency.

7️⃣ Positives & Negatives for Long-Term Investors

Positives 👍

✅ Market leader in exports with global expansion potential.

✅ Strong product pipeline in SUV & EV segments.

✅ Improving sustainability footprint (solar, rail logistics).

✅ Well-managed dealer inventory & strong rural presence.

Negatives ⚠️

⚠️ Domestic sales volume decline, especially in mini & compact cars.

⚠️ Margin pressure from commodities, forex, and new plant costs.

⚠️ Industry demand still sluggish; high reliance on SUV growth.

📌 Conclusion – Investment Stance

We maintain a Cautiously Optimistic stance. While Maruti remains a long-term structural leader in Indian PVs and is building a strong global presence, margin pressures and weak domestic demand warrant near-term caution.

For long-term investors: Gradual accumulation on dips is preferred.

Short-term traders: Monitor festive season sales & margin trends closely.

Disclosure: This analysis is provided solely for informational purposes and does not constitute investment advice. Investors should perform their own due diligence before making investment decisions.