👔 Manyavar (Vedant Fashions Ltd) Q1 FY26 Results – Steady Growth Amidst Mixed Market Sentiments

CMP: ₹749 | Sector: Wedding & Celebration Wear | Market Cap: ~₹18,000 Cr+

📰 1. Recent Insights & Highlights

Wedding Season Boost: Rebound in wedding dates compared to Q1 FY25 drove 23.2% YoY growth in customer sales.

Strong SSG: Same-store sales growth at +17.6% YoY, driven by better footfalls & higher conversions.

Category Wins:

Rajwada Collection for grooms performing well.

Mohey (women’s brand) outpacing company average in growth.

Twamev expanding premium segment presence with flagship opening in Mumbai.

Diwas preparing for festive push with e-commerce focus.

Regional Recovery: Andhra Pradesh & Telangana bounced back strongly, leading growth in Q1.

Digital Push: Aggressive influencer marketing & omni-channel integration improving reach.

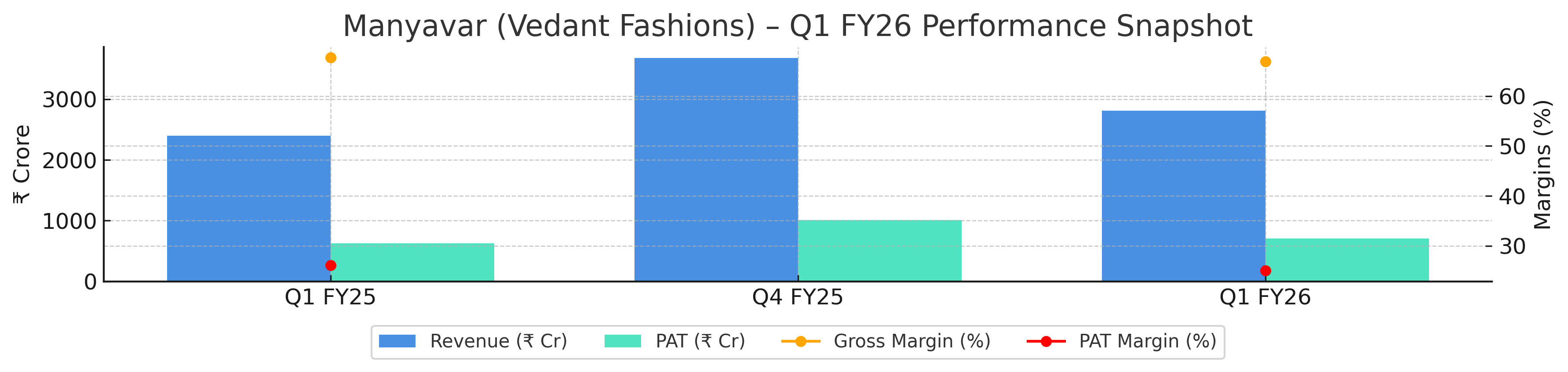

📊 2. Consolidated Financial Analysis

Segmental Performance (Retail Sales by Customers)

Total: ₹4,057 Cr (+23.2% YoY)

SSSG: +17.6% YoY

📈 3. Profitability, Growth & Valuation Ratios

EPS: ₹2.89 (vs ₹2.57 LY)

ROE & ROCE: Industry-leading (exact quarterly not disclosed, FY25 ROCE ~68.7%)

P/E: ~46x (CMP ₹749, TTM EPS ~₹16.3) – premium valuation.

Margins: Still among the highest in apparel retail despite dip.

🧵 4. Industry-Specific KPIs (Wedding & Celebration Wear)

Volume Growth: Majority of growth from volume, with slight ASP increase.

Pricing: No discount policy maintained for Manyavar brand.

Channel Mix: EBO-led expansion with selective SIS & e-commerce scale-up.

Inventory Management: Automated replenishment system at pincode level aiding efficiency.

🔍 5. FY26 Estimates Based on Trends

Past 4-quarter trend (Sales / Profit / Margin):

FY25 Sales Growth: ~+1%

FY25 Profit Growth: ~-6%

FY25 Margin: 28%

Considering Q1 FY26 performance:

Sales Growth (FY26E): ~+9% (wedding season aiding H1, cautious H2 outlook)

Profit Margins (FY26E): ~25% (higher marketing costs offsetting scale benefits)

Profit Growth (FY26E): ~-2%

🔮 6. Outlook

Near-Term (1–2 Quarters):

Expect strong festive season contribution (Q3 focus).

Continued recovery in AP & Telangana positive for sales.

Gross additions in stores at 8–10%, but with closures of underperforming outlets.

Long-Term (3–5 Years):

Strong moat in wedding wear, premiumization via Twamev, and festive segment expansion via Diwas.

Mohey well-placed to tap women’s ethnic wear growth.

Risk factors: Weak consumer sentiment in mid-premium discretionary segment, rising lease costs, competition from unorganized players.

⚖️ 7. Conclusion for Long-Term Investors

Positives ✅

Industry leader with strong brand recall.

High margins & ROCE in apparel retail.

Diversified portfolio targeting multiple customer segments.

Proven asset-light model with strong cash flows.

Negatives ⚠️

Margins dipped due to higher marketing spend (25% PAT margin vs 26.1% LY).

Valuations expensive at ~45X PE.

Consumer sentiment in mid-premium segment remains weak.

Dependence on wedding calendar seasonality.

Investment Stance: Hold with Cautious Optimism – A quality franchise, but better entry points may arise if valuations correct or macro sentiment improves.

📢 Disclosure

This analysis is provided solely for informational purposes and does not constitute investment advice. Investors should perform their own due diligence before making investment decisions.